Combo Strategy 123 Reversal & Cueing Off Sup/Res Levels This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

Cueing Off Support And Resistance Levels, by Thom Hartle

modified by HPotter for trade signals.

The related article is copyrighted material from Stocks & Commodities.

WARNING:

- For purpose educate only

- This script to change bars colors.

Search in scripts for "the strat"

Full Range Trading Study with Alerts and DCA

Introduction

This is the study version of my range trading strategy. It is designed to be a “drop in” replacement for its twin strategy. I have replicated the analysis logic and entry and exit procedures to produce a nearly identical result set to the strategy. Other than the properties tab, the inputs dialog is exactly the same. Backtest the strategy to determine the best inputs to trade. Then apply the same inputs to this study to forward test. Alerts are available for trade entry, take profit close and stop-loss exit. Please see the strategy version for a complete description of the trading behavior of this script.

In brief, this script is intended to benefit from a range bound market. The trading behavior is to buy on weakness and sell on strength. As such trade orders are placed in a counter direction to price pressure. What you will see on the chart is a short position on peaks and a long position on valleys. This is accomplished by calculating pivot points from the price stream. Rising pivots are shorts and falling pivots are longs. I refer to pivots as a vertex in the inputs dialog box. The cone based measurement adds a peak, sides and a base to the calculation elements. This allows the inputs to focus on adjusting the location of trades and not just trend lines. The pivot points can be plotted on the backtest. You can use the vertex input values to move the pivots where you want trades to be. This script can be traded in four different modes: Long, Short, BiDir, and Ping Pong. When trading in “Ping Pong” mode long and short positions are intermingled continuously as long as there exists a detectable vertex. I also have a trend following version of this script for those not interested in trading the range.

This script employs a DCA feature which enables users to experiment with loss recovery techniques in the backtest. Here in the study the summary report displays the “Debt Sequence” number which can be used to manually increase the order size on subsequent trades at the broker. The script keeps track of debt incurred from losing trades. When the debt is recovered the “Debt Sequence” resets to zero so orders can return to the base size. Be sure to set the limiter to prevent your account from depleting capital during runaway markets.

Consecutive loss limit can be set to report a breach of the threshold value. Every stop hit beyond this limit will be reported on a version 4 label above the bar where the stop is hit. Use the consecutive loss limit to manually halt live trading on the broker side.

Design

This script uses twelve indicators on a single time frame and is approximately 1800 lines of Pine 4 code. The original trading algorithms are a port from a much larger program on another trading platform. I’ve converted some of the statistical functions to use standard indicators available on TradingView. The setups make heavy use of the Hull Moving Average in conjunction with EMAs that form the Bill Williams Alligator as described in his book “New Trading Dimensions” Chapter 3. Lag between the Hull and the EMAs form the basis of the entry and exit points. The vertices are calculated using one of five featured indicators: Volume, Histogram, Fractal, Candle and Macro. The backtest is used to determine the best fit for your desired trading instrument. The incorporation of five distinct pivot point calculations broadens the scope of the markets where this tool can be beneficial.

Example configurations for various instruments along with a detailed PDF user manual is available.

Indicator Repainting

Please see the strategy script for a more detailed description of the repaint problem. The goal of my repaint prevention in the study script is simply to ensure that my signal trading bias remains consistent between the strategy, study and broker. This script employs the following conventions in effort to avoid indicator repainting:

1. This script uses only 1 time frame. The chart interval.

2. Every entry and exit condition is evaluated on closed bars only.

3. Entry and exit plots are not triggered off trend line crossovers.

4. No security functions are called to avoid a look-ahead possibility.

5. Every contributing factor specified in the TradingView wiki regarding this issue has been addressed. Except the use of the exponential moving average which is essential to my strategy.

6. I’ve run a 10 minute chart live for a week and compared it to the same chart periodically reloaded. The two charts were highly correlated with no instances of completely opposite real-time signals

This script does indeed bring up the TradingView warning dialog. The only reason for this is due to “peculiarities of the algorithm” regarding the EMA as stated in the wiki article.

The Bottom Line. Does this script repaint. Yes, it will repaint about as much as every other trading platform which combines backtest data with real time prices in a live trading scenario.

Usage

Please be aware that the purpose of the study script is to perform forward testing of the configuration established in the backtest process. Therefore, the usage here in the study begins with the backtest configuration parameters. The following steps provide instructions to get this study script connected to the TradingView alert notification system. For a detailed description of how to create a range trading system using this script please see the strategy version.

Step 1. Create a chart with the trading instrument and interval used in the backtest.

Step 2. Find this script in the “Invite Only” section of the Indicators Dialog and apply it to the current chart.

Step 3. Copy the values from the backtest input dialog to the study.

Step 4. Open the TradingView Alert window.

Step 5. In the “Condition” drop down field find and select the name of the script.

Step 6. A new drop down field will appear with the alerts available in the script. This script exposes the following six signals:

Long Entry Signal

Long Profit Signal

Long Stop-loss Signal

Short Entry Signal

Short Profit Signal

Short Stop-loss Signal

Select the signal for which you want notification.

Step 7. In the “Options” field select the frequency of the alert. Typically, "Once Per Bar" or "Once Per Bar Close" will be sufficient.

Step 8. Set the expiration date and time.

Step 9. Select the action of the alert. Currently TradingView offers six different actions:

Notify on App

Show Popup

Send Email

Webhook URL

Play Sound

Send Email to SMS

Step 10. Create a message to to transmitted with the alert. The script provides a default message which can be overridden with any custom description. The price, time and other reserved chart elements can be included in the message

Step 11. Click the “Create” button to generate this single alert.

Step 12. Repeat steps 1 through 11 for every signal you wish to receive.

This script is open for beta testing. After successful beta test it will become a commercial application available by subscription only. I’ve invested quite a lot of time and effort into making this the best possible signal generator for all of the instruments I intend to trade. I certainly welcome any suggestions for improvements. Thank you all in advance.

Combo Strategy 123 Reversal & Confluence This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

This is modified version of Dale Legan's "Confluence" indicator written by Gary Fritz.

================================================================

Here is Gary`s commentary:

Since the Confluence indicator returned several "states" (bull, bear, grey, and zero),

he modified the return value a bit:

-9 to -1 = Bearish

-0.9 to 0.9 = "grey" (and zero)

1 to 9 = Bullish

The "grey" range corresponds to the "grey" values plotted by Dale's indicator, but

they're divided by 10.

WARNING:

- For purpose educate only

- This script to change bars colors.

Combo Strategy 123 Reversal & Comparative Relative Strength This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

Comparative Relative Strength Strategy for ES

WARNING:

- For purpose educate only

- This script to change bars colors.

Combo Strategy 123 Reversal & Commodity Selection Index This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

The Commodity Selection Index ("CSI") is a momentum indicator. It was

developed by Welles Wilder and is presented in his book New Concepts in

Technical Trading Systems. The name of the index reflects its primary purpose.

That is, to help select commodities suitable for short-term trading.

A high CSI rating indicates that the commodity has strong trending and volatility

characteristics. The trending characteristics are brought out by the Directional

Movement factor in the calculation--the volatility characteristic by the Average

True Range factor.

Wilder's approach is to trade commodities with high CSI values (relative to other

commodities). Because these commodities are highly volatile, they have the potential

to make the "most money in the shortest period of time." High CSI values imply

trending characteristics which make it easier to trade the security.

The Commodity Selection Index is designed for short-term traders who can handle

the risks associated with highly volatile markets.

WARNING:

- For purpose educate only

- This script to change bars colors.

Combo Strategy 123 Reversal & EMA & Volume Weighting This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

The related article is copyrighted material from Stocks & Commodities 2009 Oct

WARNING:

- For purpose educate only

- This script to change bars colors.

Combo Strategy 123 Reversal & DMI & Moving Average This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

The related article is copyrighted material from Stocks & Commodities Aug 2009

Combining DMI And Moving Average Trading System

WARNING:

- For purpose educate only

- This script to change bars colors.

Cyatophilum H.A. Swing [ALERT SETUP]Hi guys, to celebrate the beginning of a new altcoins cycle, I created a Swing trade Indicator. (It's a joke, there will not be any altcoins cycle)

Cyatophilum Heikin Ashi Swing

This indicator will allow us to create one strategy for each pair and never miss those big swings ever again!

HOW BEAT BUY & HOLD WORKS

This kind of strategy is a safe long term investment , usually played in high timeframes such as 4H, 1D etc.

It is perfect for beginners in trading as the process is very simple: buy and sell when you receive the alert. The high timeframes allows to trade manually by receiving alerts on your phone or email, but you also can automate it if you prefer.

The primary goal of these strategies is to increase your capital faster than someone simply holding the asset .

The trades are made with no leverage and 100% equity . It is for those who want to grow their portfolio fast without risking to lose everything. You can use several strategies at once, in this case split your equity accordingly.

HOW DOES IT WORK?

The Heikin Ashi candles are very usefull. This strategy is built upon H.A. candles but is used on normal candles, because H.A. candles price are an average of real candles and we want to know the real price. I did the trick by recalculating the H.A. open, high, low and close with the original formula based on the real candles's ohlc. This allows me to use the strategy tester and backtest with real results.

HOW TO USE

Creating a signal is as simple as adding the indicator called to your chart and click "Set alert". Select "Once per bar close" for your alert options.

There are 3 alerts:

- BUY

- SELL

- BUY OR SELL (for free TV users)

Sample Backtest results

Bitcoin/Dollar

Ethereum/Bitcoin

Basic Attention Token/Bitcoin

> > Start using the indicator now < <

Note: This version is the ALERT SETUP. You can find the Backtest version on my profile scripts.

Combo Strategy 123 Reversal & CMOfilt This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

This indicator plots a CMO which ignores price changes which are less

than a threshold value. CMO was developed by Tushar Chande. A scientist,

an inventor, and a respected trading system developer, Mr. Chande developed

the CMO to capture what he calls "pure momentum". For more definitive

information on the CMO and other indicators we recommend the book The New

Technical Trader by Tushar Chande and Stanley Kroll.

The CMO is closely related to, yet unique from, other momentum oriented

indicators such as Relative Strength Index, Stochastic, Rate-of-Change, etc.

It is most closely related to Welles Wilder`s RSI, yet it differs in several ways:

- It uses data for both up days and down days in the numerator, thereby directly

measuring momentum;

- The calculations are applied on unsmoothed data. Therefore, short-term extreme

movements in price are not hidden. Once calculated, smoothing can be applied to the

CMO, if desired;

- The scale is bounded between +100 and -100, thereby allowing you to clearly see

changes in net momentum using the 0 level. The bounded scale also allows you to

conveniently compare values across different securities.

WARNING:

- For purpose educate only

- This script to change bars colors.

Combo Strategy 123 Reversal & CMOavThis is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

This indicator plots average of three different length CMO's. This indicator

was developed by Tushar Chande. A scientist, an inventor, and a respected

trading system developer, Mr. Chande developed the CMO to capture what he

calls "pure momentum". For more definitive information on the CMO and other

indicators we recommend the book The New Technical Trader by Tushar Chande

and Stanley Kroll.

The CMO is closely related to, yet unique from, other momentum oriented

indicators such as Relative Strength Index, Stochastic, Rate-of-Change, etc.

It is most closely related to Welles Wilder?s RSI, yet it differs in several ways:

- It uses data for both up days and down days in the numerator, thereby directly

measuring momentum;

- The calculations are applied on unsmoothed data. Therefore, short-term extreme

movements in price are not hidden. Once calculated, smoothing can be applied to

the CMO, if desired;

- The scale is bounded between +100 and -100, thereby allowing you to clearly see

changes in net momentum using the 0 level. The bounded scale also allows you to

conveniently compare values across different securities.

WARNING:

- For purpose educate only

- This script to change bars colors.

Combo Strategy 123 Reversal & CMOabs This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

This indicator plots the absolute value of CMO. CMO was developed by Tushar

Chande. A scientist, an inventor, and a respected trading system developer,

Mr. Chande developed the CMO to capture what he calls "pure momentum". For

more definitive information on the CMO and other indicators we recommend the

book The New Technical Trader by Tushar Chande and Stanley Kroll.

The CMO is closely related to, yet unique from, other momentum oriented indicators

such as Relative Strength Index, Stochastic, Rate-of-Change, etc. It is most closely

related to Welles Wilder`s RSI, yet it differs in several ways:

- It uses data for both up days and down days in the numerator, thereby directly

measuring momentum;

- The calculations are applied on unsmoothed data. Therefore, short-term extreme

movements in price are not hidden. Once calculated, smoothing can be applied to

the CMO, if desired;

- The scale is bounded between +100 and -100, thereby allowing you to clearly see

changes in net momentum using the 0 level. The bounded scale also allows you to

conveniently compare values across different securities.

WARNING:

- For purpose educate only

- This script to change bars colors.

Combo Strategy 123 Reversal & CMO & WMA This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

This indicator plots Chandre Momentum Oscillator and its WMA on the

same chart. This indicator plots the absolute value of CMO.

The CMO is closely related to, yet unique from, other momentum oriented

indicators such as Relative Strength Index, Stochastic, Rate-of-Change,

etc. It is most closely related to Welles Wilder?s RSI, yet it differs

in several ways:

- It uses data for both up days and down days in the numerator, thereby

directly measuring momentum;

- The calculations are applied on unsmoothed data. Therefore, short-term

extreme movements in price are not hidden. Once calculated, smoothing

can be applied to the CMO, if desired;

- The scale is bounded between +100 and -100, thereby allowing you to clearly

see changes in net momentum using the 0 level. The bounded scale also allows

you to conveniently compare values across different securities.

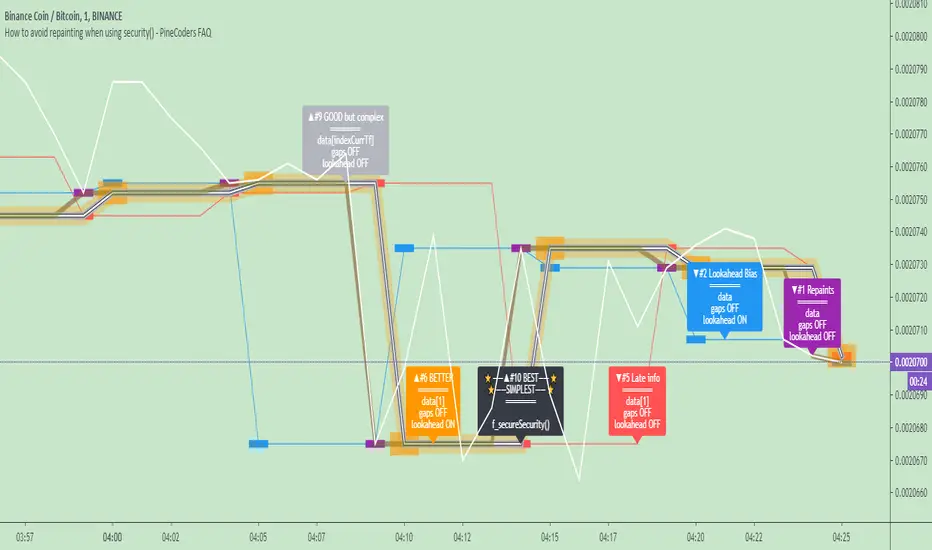

How to avoid repainting when using security() - PineCoders FAQNOTE

The non-repainting technique in this publication that relies on bar states is now deprecated, as we have identified inconsistencies that undermine its credibility as a universal solution. The outputs that use the technique are still available for reference in this publication. However, we do not endorse its usage. See this publication for more information about the current best practices for requesting HTF data and why they work.

This indicator shows how to avoid repainting when using the security() function to retrieve information from higher timeframes.

What do we mean by repainting?

Repainting is used to describe three different things, in what we’ve seen in TV members comments on indicators:

1. An indicator showing results that change during the realtime bar, whether the script is using the security() function or not, e.g., a Buy signal that goes on and then off, or a plot that changes values.

2. An indicator that uses future data not yet available on historical bars.

3. An indicator that uses a negative offset= parameter when plotting in order to plot information on past bars.

The repainting types we will be discussing here are the first two types, as the third one is intentional—sometimes even intentionally misleading when unscrupulous script writers want their strategy to look better than it is.

Let’s be clear about one thing: repainting is not caused by a bug ; it is caused by the different context between historical bars and the realtime bar, and script coders or users not taking the necessary precautions to prevent it.

Why should repainting be avoided?

Repainting matters because it affects the behavior of Pine scripts in the realtime bar, where the action happens and counts, because that is when traders (or our systems) take decisions where odds must be in our favor.

Repainting also matters because if you test a strategy on historical bars using only OHLC values, and then run that same code on the realtime bar with more than OHLC information, scripts not properly written or misconfigured alerts will alter the strategy’s behavior. At that point, you will not be running the same strategy you tested, and this invalidates your test results , which were run while not having the additional price information that is available in the realtime bar.

The realtime bar on your charts is only one bar, but it is a very important bar. Coding proper strategies and indicators on TV requires that you understand the variations in script behavior and how information available to the script varies between when the script is running on historical and realtime bars.

How does repainting occur?

Repainting happens because of something all traders instinctively crave: more information. Contrary to trader lure, more information is not always better. In the realtime bar, all TV indicators (a.k.a. studies ) execute every time price changes (i.e. every tick ). TV strategies will also behave the same way if they use the calc_on_every_tick = true parameter in their strategy() declaration statement (the parameter’s default value is false ). Pine coders must decide if they want their code to use the realtime price information as it comes in, or wait for the realtime bar to close before using the same OHLC values for that bar that would be used on historical bars.

Strategy modelers often assume that using realtime price information as it comes in the realtime bar will always improve their results. This is incorrect. More information does not necessarily improve performance because it almost always entails more noise. The extra information may or may not improve results; one cannot know until the code is run in realtime for enough time to provide data that can be analyzed and from which somewhat reliable conclusions can be derived. In any case, as was stated before, it is critical to understand that if your strategy is taking decisions on realtime tick data, you are NOT running the same strategy you tested on historical bars with OHLC values only.

How do we avoid repainting?

It comes down to using reliable information and properly configuring alerts, if you use them. Here are the main considerations:

1. If your code is using security() calls, use the syntax we propose to obtain reliable data from higher timeframes.

2. If your script is a strategy, do not use the calc_on_every_tick = true parameter unless your strategy uses previous bar information to calculate.

3. If your script is a study and is using current timeframe information that is compared to values obtained from a higher timeframe, even if you can rely on reliable higher timeframe information because you are correctly using the security() function, you still need to ensure the realtime bar’s information you use (a cross of current close over a higher timeframe MA, for example) is consistent with your backtest methodology, i.e. that your script calculates on the close of the realtime bar. If your system is using alerts, the simplest solution is to configure alerts to trigger Once Per Bar Close . If you are not using alerts, the best solution is to use information from the preceding bar. When using previous bar information, alerts can be configured to trigger Once Per Bar safely.

What does this indicator do?

It shows results for 9 different ways of using the security() function and illustrates the simplest and most effective way to avoid repainting, i.e. using security() as in the example above. To show the indicator’s lines the most clearly, price on the chart is shown with a black line rather than candlesticks. This indicator also shows how misusing security() produces repainting. All combinations of using a 0 or 1 offset to reference the series used in the security() , as well as all combinations of values for the gaps= and lookahead= parameters are shown.

The close in the call labeled “BEST” means that once security has reached the upper timeframe (1 day in our case), it will fetch the previous day’s value.

The gaps= parameter is not specified as it is off by default and that is what we need. This ensures that the value returned by security() will not contain na values on any of our chart’s bars.

The lookahead security() to use the last available value for the higher timeframe bar we are using (the previous day, in our case). This ensures that security() will return the value at the end of the higher timeframe, even if it has not occurred yet. In our case, this has no negative impact since we are requesting the previous day’s value, with has already closed.

The indicator’s Settings/Inputs allow you to set:

- The higher timeframe security() calls will use

- The source security() calls will use

- If you want identifying labels printed on the lines that have no gaps (the lines containing gaps are plotted using very thick lines that appear as horizontal blocks of one bar in length)

For the lines to be plotted, you need to be on a smaller timeframe than the one used for the security() calls.

Comments in the code explain what’s going on.

Look first. Then leap.

Combo Strategy 123 Reversal & Chande Momentum OscillatorThis is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

This indicator plots Chande Momentum Oscillator. This indicator was

developed by Tushar Chande. A scientist, an inventor, and a respected

trading system developer, Mr. Chande developed the CMO to capture what

he calls "pure momentum". For more definitive information on the CMO and

other indicators we recommend the book The New Technical Trader by Tushar

Chande and Stanley Kroll.

The CMO is closely related to, yet unique from, other momentum oriented

indicators such as Relative Strength Index, Stochastic, Rate-of-Change,

etc. It is most closely related to Welles Wilder`s RSI, yet it differs

in several ways:

- It uses data for both up days and down days in the numerator, thereby

directly measuring momentum;

- The calculations are applied on unsmoothed data. Therefore, short-term

extreme movements in price are not hidden. Once calculated, smoothing

can be applied to the CMO, if desired;

- The scale is bounded between +100 and -100, thereby allowing you to

clearly see changes in net momentum using the 0 level. The bounded scale

also allows you to conveniently compare values across different securities.

WARNING:

- For purpose educate only

- This script to change bars colors.

Combo Strategy 123 Reversal & Chande Forecast Oscillator This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

The Chande Forecast Oscillator developed by Tushar Chande The Forecast

Oscillator plots the percentage difference between the closing price and

the n-period linear regression forecasted price. The oscillator is above

zero when the forecast price is greater than the closing price and less

than zero if it is below.

WARNING:

- For purpose educate only

- This script to change bars colors.

Combo Strategy 123 Reversal & Chaikin Volatility This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

Chaikin's Volatility indicator compares the spread between a security's

high and low prices. It quantifies volatility as a widening of the range

between the high and the low price.

You can use in the xPrice1 and xPrice2 any series: Open, High, Low, Close, HL2,

HLC3, OHLC4 and ect...

WARNING:

- For purpose educate only

- This script to change bars colors.

Combo Strategy 123 Reversal & Center Of Gravity This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

The indicator is based on moving averages. On the basis of these, the

"center" of the price is calculated, and price channels are also constructed,

which act as corridors for the asset quotations.

WARNING:

- For purpose educate only

- This script to change bars colors.

Combo Strategy 123 Reversal & CCI This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

The Commodity Channel Index (CCI) is best used with markets that display cyclical or

seasonal characteristics, and is formulated to detect the beginning and ending of these

cycles by incorporating a moving average together with a divisor that reflects both possible

and actual trading ranges. The final index measures the deviation from normal, which indicates

major changes in market trend.

To put it simply, the Commodity Channel Index (CCI) value shows how the instrument is trading

relative to its mean (average) price. When the CCI value is high, it means that the prices are

high compared to the average price; when the CCI value is down, it means that the prices are low

compared to the average price. The CCI value usually does not fall outside the -300 to 300 range

and, in fact, is usually in the -100 to 100 range.

WARNING:

- For purpose educate only

- This script to change bars colors.

kiska cloudskiska clouds: crypto twitter's next cloud meme

Crypto is a fast-paced, highly-volatile asset, therefore, many traditional strategies are thrown out of the window when applied to cryptocurrency markets. In trading, there are only two things known for sure: price and volume. Price and volume data is then manipulated using various math equations in an effort to discover patterns and/or make predictions. kiska clouds are no different.

The kiska clouds are a simple crossover strategy. The clouds are different because of the unique averages being used and the embedded momentum indicator.

To use the clouds is simple:

When the green line crosses above the pink line, you buy/long.

When the green line crosses below the pink line, you sell/short.

The clouds are indicative of the trend's momentum. Using the power of math, the larger the cloud indicates a higher amount of buying/selling pressure. As the cloud thins, momentum is slowing, and the trend may be reversing.

At the time of testing, the strategy had a profitability of 54.55% accuracy with 1133.41% net profit. While I think this could be automated into a bot, adding a human element with stop losses and further analysis will significantly improve the accuracy/profitability.

This indicator is a "Pay What You Want" model. For a trial or to purchase this indicator, send me a message on Twitter @moonkiska or here on TradingView. You will be granted a 2-3 day trial period to the backtesting strategy.

Tips:

The higher the time frame, the more accurate the strategy.

Personally, I do not short above the 200MA. I do not long below the 200MA.

Coming Soon:

Support/Resistance

Trend Lines

Combo Strategy 123 Reversal & Bull Power This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

Bull Power Indicator

To get more information please see "Bull And Bear Balance Indicator"

by Vadim Gimelfarb.

WARNING:

- For purpose educate only

- This script to change bars colors.

Combo Strategy 123 Reversal & Bull And Bear Balance This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

This new indicator analyzes the balance between bullish and

bearish sentiment.

One can cay that it is an improved analogue of Elder Ray indicator.

To get more information please see "Bull And Bear Balance Indicator"

by Vadim Gimelfarb.

WARNING:

- For purpose educate only

- This script to change bars colors.

Combo Strategy 123 Reversal & Breakout Range Short This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

Breakout Range Short Strategy

WARNING:

- For purpose educate only

- This script to change bars colors.

Combo Strategy 123 Reversal & Breakout Range Long This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

Breakout Range Long Strategy

WARNING:

- For purpose educate only

- This script to change bars colors.